Fate of Money is Here: Investigating Fintech Industry Patterns

The fate of money is being formed by fintech patterns, and the worth of the worldwide fintech applications’ market is assessed to hit $305 billion by 2025. That is a colossal number contrasted with its simple 11 million dollar valuation in 2010. The immense contrast just denotes the beginning of the frenzy set off among youthful fintech undertakings and fintech designers associated with Programming Advancement For New companies.

Today, numerous fintech applications are now coming to the standard market. The business is going through different patterns right now. A considerable lot of these patterns are as of now coursing and are supposed to lead in 2024. In any case, before we adventure into these patterns, how about we comprehend Fintech and what it involves.

What is Fintech?

A portmanteau word for money and innovation, Fintech is exactly what lies under the surface for it innovation driven finance. The fintech business contains all product, innovation, or applications that utilize innovation to work with finance in additional ways than one. Fintech applications are utilized for different capabilities, including biometric validation, multi-client cooperation, cross-stage combinations, investigation and information perception, numerous installment entryways, and that’s only the tip of the iceberg.

Fintech applications are likewise extraordinary imagination and advancement instruments for designers and business people the same. An assortment of fintech projects have proactively been sent off on the lookout. The kinds of fintech applications incorporate versatile banking applications, protection applications, e-wallets, exchanging stages, and that’s just the beginning. The following are a couple other fintech industry drifts that are picking up speed and are supposed to govern in 2024.

9 Must-Know FinTech Patterns for 2024-2025

Inserted Money

NeoBanking

Regtech Arrangement

Mechanical Cycle Mechanization (RPAs)

CBDCs

BNPL

Computerized Character Confirmation

Computerized reasoning

OpenBanking

Installed Money

As the name proposes, installed finance alludes to coordinating monetary administrations, for example, loaning, installment handling, or protection into existing non-monetary applications and working frameworks. The hunt volume related with the word ‘inserted finance’ has soar. This is on the grounds that organizations are gradually understanding the advantages of the computerized change of fintech frameworks. Organizations ought to know about unambiguous classes of implanted finance. As per a report by Detonating Subjects, the inserted fintech market is esteemed at $63.2 billion and is anticipated to develop to more than $248 billion by 2032.

We should view these classifications and their models.

Implanted installments

Implanted installment entrances could be viewed as the most widely recognized kind of inserted finance application. Instances of implanted installment outlets remember entryways for Amazon, Uber, Walmart, and Zomato applications. Other inserted installment frameworks incorporate Google Pay, Apple Pay, and BHIM, which store data and work with exchanges.

Implanted loaning

One more class of installed finance is inserted loaning. Implanted loaning eliminates the need to depend on banks and other monetary establishments as delegates. The actual applications mechanize the loaning of immense measures of capital at less expense and time.

The organizations can get to cash from solid SaaS organizations straight away. This has prompted an uncommon expansion popular for a solid Portable Application Improvement Organization which grows such SaaS arrangements. This is by all accounts an extremely rewarding industry and is supposed to be valued at $7trillion inside the following decade.

NeoBanking

Neobank is an immediate bank working totally internet banking without conventional financial organizations. A neobank is a sort of trendy bank with practically no actual area and is by and by completely on the web. Such banks give versatile first monetary answers for installments, cash moves, loaning, and then some.

These banks likewise permit clients to put aside installments, pull out cash, and even credit and loaning administrations. This implies the administrations are only equivalent to conventional banks offer. In any case, one downside to neo banks is that they need banking licenses and can’t work independent.

Regtech Arrangement

Regtech arrangements are additionally kinds of fintech items that are utilized to oversee administrative cycles through innovation. The elements of such arrangements are principally guidelines checking, revealing, and consistence.

RegTech is the administration of administrative cycles through innovation, typically inside the monetary business. Its primary highlights incorporate administrative checking, revealing, and consistence. RegTech comprises of organizations that utilization distributed computing advancements through SaaS to assist organizations with conforming to guidelines. It is known as administrative innovation.

Mechanical Interaction Computerization (RPAs)

Another pattern that is getting on in the fintech business are RPAs. Mechanical interaction mechanization (RPA) is a product innovation that empowers simple sending and the executives of programming robots that imitate human activities while drawing in with computerized frameworks and programming.

RPA programming is instrumental in building robots that can translate pictures, explore frameworks, distinguish and separate information, characterize activities, and more while conveying improved productivity and cost-adequacy than human partners. In a review by Gartner, RPA was distinguished as the quickest developing fragment in the worldwide programming market. With an expected 63% development rate(Gartner) in 2018 and, surprisingly, more in the last 1.5 years, the pattern is in essence set to dramatically develop.

CBDCs

National Bank Computerized Money, also known as CBDCs, is another Fintech pattern to keep an eye out for. CBDCs are computerized cash gave by a country’s national bank. National bank computerized monetary standards are a type of computerized money that is comparable to the worth of official government issued money. CBDCs are acquiring ubiquity as they decrease the gamble related with utilizing advanced monetary forms or digital currencies. While digital forms of money are profoundly unstable in esteem, that is not the situation with CBDCs, which have a decent worth and exceptionally low unpredictability. This is on the grounds that the national bank of that nation controls them.

BNPL

Purchase Presently, Pay Later or BNPL is a classification of transient term funding that empowers clients to buy while paying for it in portions after the buy. This is very like EMI choices on any buy. The valuation of the BNPL market flooded to 120 billion bucks somewhere in the range of 2019 and 2021. That is very nearly a CAGR of 85%, checking gigantic potential for this pattern.

BNPL designs likewise charge very little or no interest. Contrasted with conventional credit lines and advances, BNPL credits are likewise effectively authorized and don’t influence FICO assessments assuming that the installments are appropriately made on time.

Computerized Personality Confirmation

Computerized Character confirmation is a strategy to give hearty safety efforts to fintech applications. This method utilizes advances, for example, multifaceted verification, twofold encryption strategies, biometric validation, and that’s just the beginning. These advances safeguard against fake exercises, cyberattacks, and unapproved admittance to monetary exchanges in the fintech scene.

Advanced characters are additionally safer than customary on-paper distinguishing proof as the archives are carefully put away internet based through rigid validation conventions. To put it plainly, computerized character check is tied in with utilizing innovation to approve an individual’s personality carefully and is ending up an aid for the fintech business.

Computerized reasoning

All enterprises are understanding the advantages of computer based intelligence in everyday tasks, and the fintech business is no exemption. Client care chatbots and imaginative computer based intelligence devices to mechanize fintech work processes are a portion of the manners in which artificial intelligence is being executed in the business. Ordinary utilization of artificial intelligence in monetary establishments has prompted as numerous as 80% of worldwide fintech organizations understanding the significance and advantages.

Most banks overall are now in the early phases of this progress and are making awesome of simulated intelligence in practically all perspectives and saving expenses. Computerization with artificial intelligence is supposed to save organizations as much as 70$ billion in North America alone. Increasing it by the quantity of nations effectively utilizing computer based intelligence procedures, cost saving emerges to be a critical number.

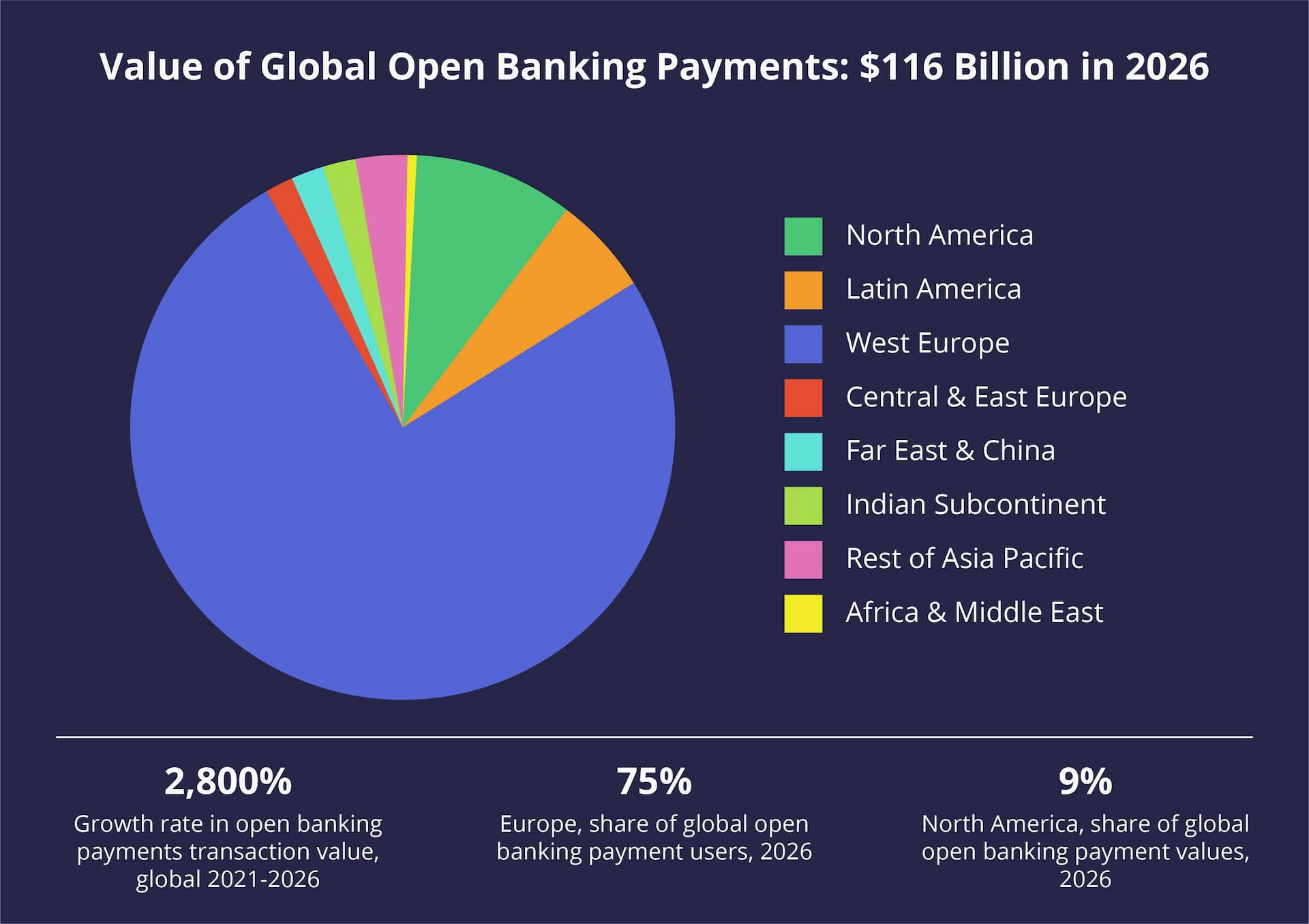

OpenBanking

Open Financial alludes to sharing monetary data to different organizations typically to support the client. Open Banking permits monetary administrations and new monetary items to its clients at the most brief notification. This not just drives contest among banks while working on the nature of administrations delivered yet additionally assist keeps money with making a superior client persona in view of the total of information from various monetary sources. This assists manages an account with cutting misfortunes and offer better types of assistance.

Key Focal points on Fintech Patterns

The fate of the Fintech business is perhaps of the main partner in the product improvement industry. Because of its high-esteem exchanges and expanded security necessities, the business likewise drives advancement in programming improvement.

While additional ventures are putting resources into fintech improvement, an ever increasing number of engineers are likewise enhancing to give greater security and straightforwardness to fintech stages. As we explore through the consistently changing FinTech Patterns, it becomes vital for stay ahead in development.

Many organizations offer monetary programming improvement yet nobody does it like OpenXcell. For Fintech Programming Improvement Organization, OpenXcell is a great accomplice for any endeavor searching for fintech programming arrangements. Its client list of 700+ blissful clients and 1000+ fruitful activities is just proof of its obligation to quality.